Deceptive dividends

Deceptive dividends

“False as wooden teeth, but the suckers are falling for it.”

Here’s a story from last week’s New York Times: Corporate America’s Chief Critic, Carl Icahn, Gets His Comeuppance

In May, Hindenburg published research suggesting that Icahn Enterprises was valued more highly than its peers because it paid a lucrative dividend to shareholders despite reporting quarterly losses, which kept investors buying the stock. “Icahn has been using money taken in from new investors to pay out dividends to old investors,” Mr. Anderson wrote, comparing it to a “Ponzi-like economic structure” that was unsustainable.

Mr. Anderson also suggested that if Icahn Enterprises stopped paying dividends, the value of its stock would fall, which meant that Mr. Icahn would struggle to repay billions of dollars he had borrowed against his personal stake in the company.

What should we make of this news? I’ll walk through some numbers with you, but first, let me describe a scene from the 1937 film Toast of New York (starring Cary Grant), which portrays (with considerable artistic license) the amazing careers of James Fisk1, Daniel Drew2, and Cornelius Vanderbilt3. This scene is just one of many in the movie which dramatizes important financial concepts.4

The Toast of New York

Starting around minute 43 of the movie, Fisk cooks up a scheme to manipulate the price of Erie Railroad:

“First, we’ll declare a dividend, the biggest declared by any railroad. Let’s say 50%.”

The tight-fisted Drew, in charge of the railroad’s finances, is initially aghast.

“50%? I ain’t got no money in the treasury for that.”

Eventually, Drew agrees to the scheme. When the dividend is announced, chaos erupts on the trading floor of the stock exchange. One trader says, in amazement,

“Who ever heard of a 50% dividend?”

His companion replies

“Nobody, but it makes Erie the best buy in the market!”

The announcement causes Erie’s stock price to surge. Vanderbilt, observing the mayhem on the trading floor, acidly comments

“I didn’t think Drew was smart enough to find a new way to start a bull rush. I’m going to fight him, go ahead and buy.”

Vanderbilt’s henchman is shocked:

“But it’s a false price!”

Vanderbilt replies

“False as wooden teeth, but the suckers are falling for it.”

Here’s wikipedia describing what happens next:

In 1866 to 1868, Drew engaged in the Erie War, in which Drew conspired along with fellow directors James Fisk and Jay Gould to issue stock to keep Vanderbilt from gaining control of the Erie Railroad. Vanderbilt, unaware of the increase in outstanding shares, kept buying Erie stock and sustained heavy losses, eventually conceding control of the railroad to the trio.

So to summarize, this example demonstrates

Sometimes shareholders like dividends (“it makes Erie the best buy in the market!”)

Dividends can confuse naive investors (“False as wooden teeth, but the suckers are falling for it.”)

There can be a connection between dividend and issuance: Drew used dividends to lure Vanderbilt in, then issued stock (Vanderbilt: “unaware of the increase in outstanding shares”).

Shareholders sometimes like dividends

Drew and Fisk are engaged in “catering”, which is described by Baker and Wurgler (2004) link as

for either psychological or institutional reasons, some investors have an uninformed and perhaps time-varying demand for dividend-paying stocks…managers rationally cater to investor demand—they pay dividends when investors put higher prices on payers, and they do not pay when investors prefer nonpayers.

Firms pay dividends because they believe retail investors like dividends, according to Brav, Graham, Harvey, Michaely (2003) link

Financial executives believe that retail investors have a strong preference for dividends, in spite of the tax disadvantage relative to repurchases.

Dividends can confuse naive investors

Let me give two examples from around 2013, a time when some claimed dividends were being overvalued by US investors, leading to an alleged dividend bubble.

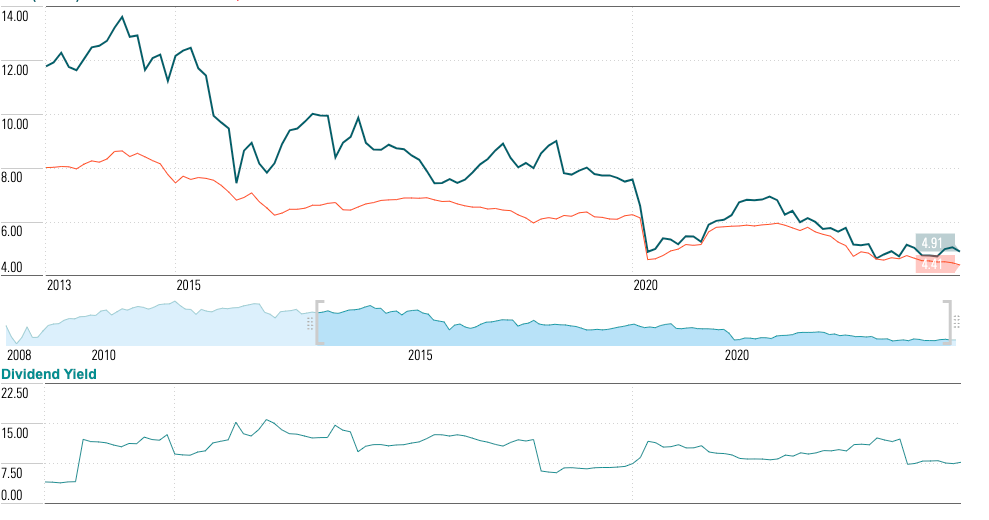

PIMCO High Income Fund

The PIMCO High Income Fund (PHK) is a closed-end fund investing in bonds. The top part of the graph below shows the price (green line) vs. NAV (orange line) of the fund. Back in 2013, the fund had a premium of around 50%, because the price was $12 while the NAV was only $8.

This premium persisted for many years, ending around 2020. Why did the fund have a premium? One explanation is its high dividend yield ,showed in the bottom graph. For many years PHK paid a constant dividend of $1.46 a year. So at a price of $8 in 2013, it had an attractive dividend yield of 12%. As the graph shows, the dividend yield remained in double digits for years.

Even today, this fund has as a premium around 11%, perhaps due to its still high dividend yield of 12%.

Here, I think we can say investors are confused by the dividend and paying too much for this fund, spending $12 on assets worth only $8.

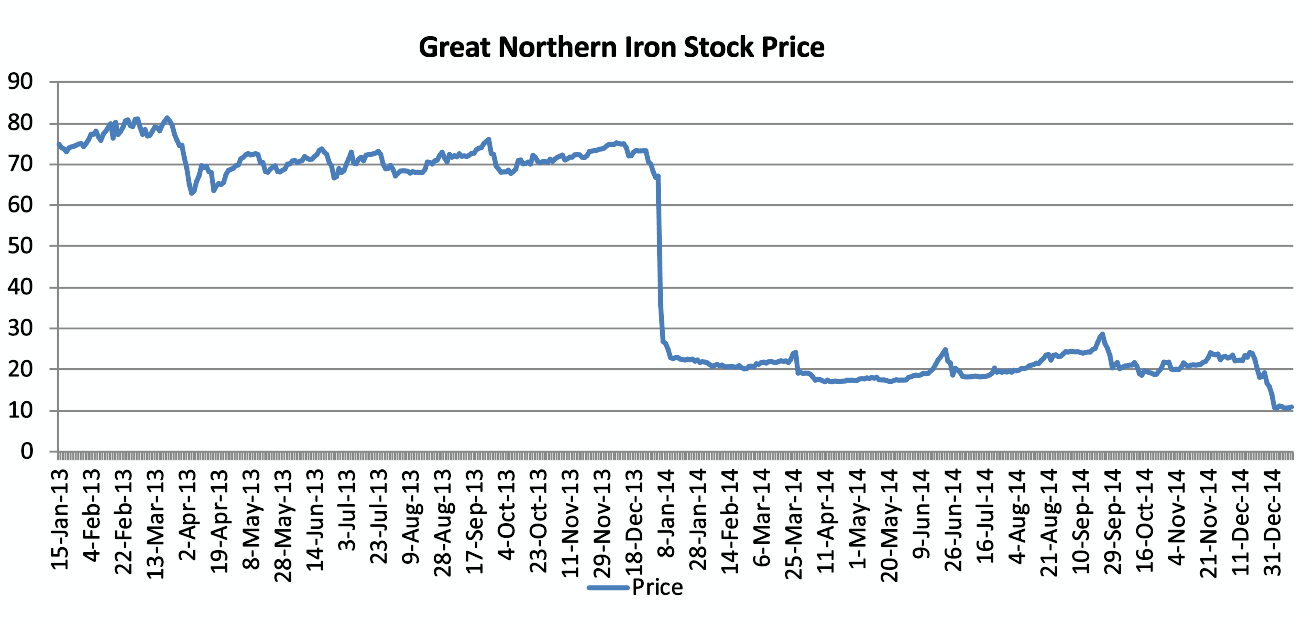

Great Northern Iron

Great Northern Iron Ore Properties (GNI) was an NYSE stock.5 As of December 2012, GNI had an attractive dividend yield of 27%. Pretty sweet!

Then around January 2014, the price plummeted from $70ish to $20ish. Ouch! But, not to worry, since in December 2014, GNI had a whopping big dividend yield of 44% according to the standard method of calculating. So who cares if the price falls, we still have that beautiful dividend, right? Remember that guy in the movie who asked "Who ever heard of a 50% dividend?" Well, GNI shareholders heard of a dividend yield of 44%, that’s who!

Unfortunately, this supposed dividend yield of 44% was not what it seemed. In April 2015 after paying one last dividend of $1.30, GNI ceased to exist and the price went to zero. What happened?

GNI was not a real company, or at least it was not a normal corporation like Apple or Microsoft or most other US stocks. Instead, it was a trust, set up in 1906 for complicated legal reasons that we don’t need to discuss but if you really must know about the Hepburn Act of 1906, see here. In any event, the trust was required to dissolve 20 years after the death of all 18 people named in the trust document, the last of whom (Louis W. Hill Jr.) died on April 6, 1995.6

Thus, the fact that GNI would go to zero in April 2015, but would be legally obligated to pay dividends from lease income it received until then, was public information since 1995. GNI was a “wasting asset” or “exhaustible resource”, like a coal mine that would run out of coal precisely on schedule in April 2015.

Yet somehow investors were treating GNI like a normal stock with underlying assets and an indefinite future, when in fact it was actually a finite stream of fairly certain dividend payments terminating in April 2015.

Armed with this information, what can we say about the price graph above?

GNI was absurdly overpriced prior to December 2013. The abrupt fall in price around January 2014 was a rational correction which pushed the price down to where it should have been the whole time.

You could also describe this price correction as delayed reaction or stale news, although the news was 20 years stale.

Perhaps the overpricing reflects investors who just like dividends without thinking about terminal values.

I’d call GNI an example of “terminal value neglect” in that investors were ignoring the public information that GNI had a terminal value of zero as of April 2015. “It's long been believed that some unwitting investors looking for yield buy GNI without studying the underlying documentation.”

I’ll have more to say about “terminal value neglect” some other time, but for now:

We see this same pattern in the often absurd overvaluation of bankrupt firms such as Bed Bath and Beyond which is “theoretically worthless”.

Similarly, nearly worthless Chinese warrants looked overpriced according to Xiong, Yu (2011), The Chinese Warrants Bubble.

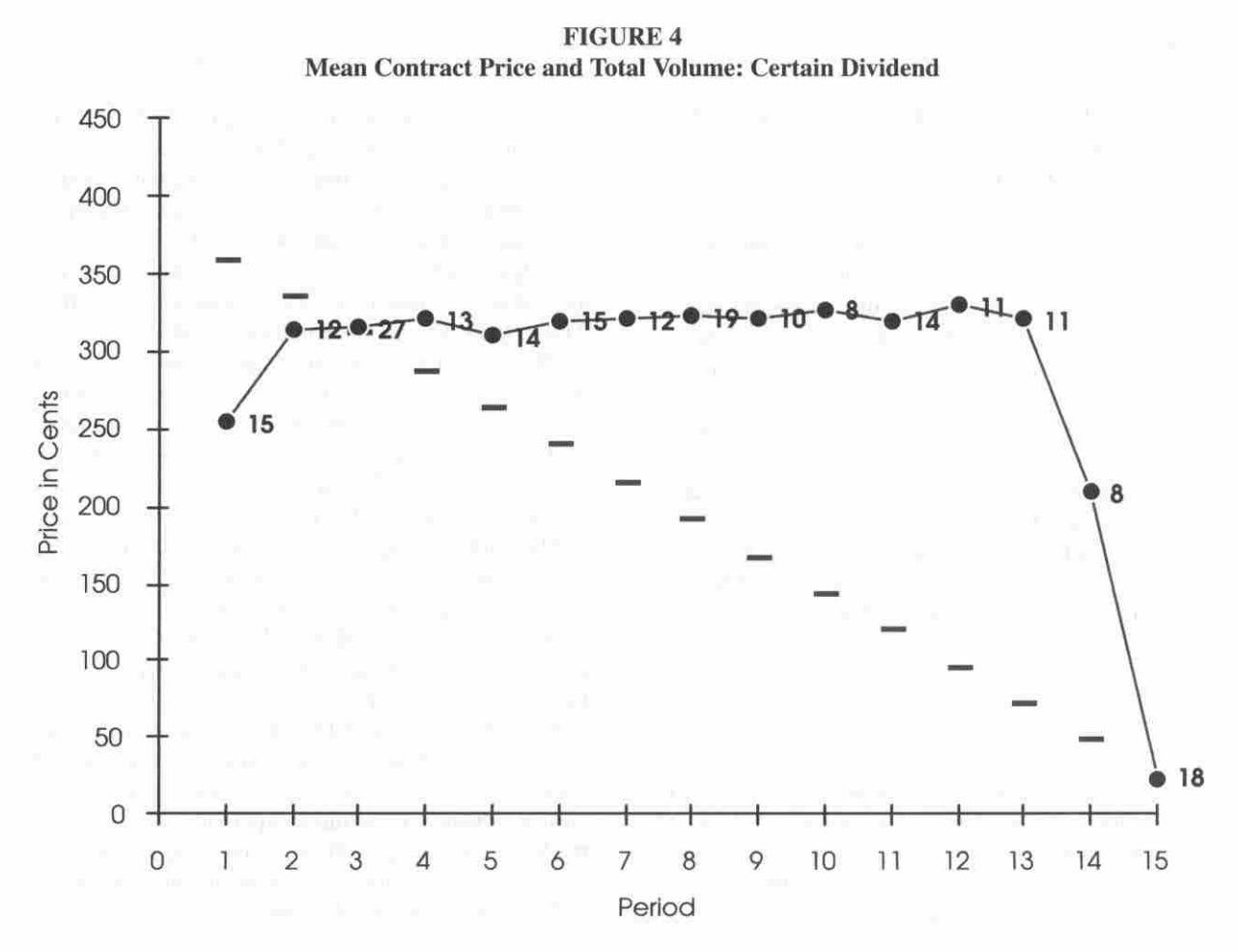

Last, the following graph looks an awful lot like GNI. It comes from Porter, Smith (2003), Stock market bubbles in the laboratory, link. The numbers in the figure show the volume traded. The flat line segments show the rational price, reflecting the deterministic future divided stream. Here is another (experimental) market with known terminal date, no uncertainty about dividends, and yet the market price seems to ignore the terminal date until suddenly falling like Wile E. Coyote.

The connection between dividends and issuance

What’s the connection between dividends and issuance? Issuance is money flowing from investors to the firm, while the dividend is money flowing from firm to investors. So if we want to look at the net cash being distributed by the firm to investors, we need to keep track of both dividends and issuance (or its opposite, repurchases).

How could Vanderbilt have avoided being swindled by Fisk and Drew?7 Vanderbilt should have checked the number of shares issued by Erie.8 Specifically, Vanderbilt could have compared the dollar dividend paid by Erie to the dollar issuance absorbed by Erie using the following formula from Goyal, Welch (2008) RFS A Comprehensive Look at the Empirical Performance of Equity Premium Prediction and Boudouck, Michaely, Richardson, Roberts (2007) JF, On the Importance of Measuring Payout Yield: Implications for Empirical Asset Pricing, link, I show the Boudouck et al version here:

The above formula is measured in dollars and all you need to calculate issuance is market cap and capital gain return, RETX. In an ideal world, we would calculate this number monthly or daily, but for the sake of exposition, let me calculate it annually. Here I taking some short cuts but let us just make a rough approximate calculation.

As of December 2022, Icahn Enterprises (IEP) had a conventionally defined dividend yield of 15.8%. Is this high or low? Let us compare it to the annual net issuance calculated using the above formula. In order to make net issuance into a yield similar to dividend yield, I will just divide by December 2022 market cap.

Let us evaluate using annual data, comparing December 2022 to December 2021. For both calendar years 2022, and 2021, IEP paid an annual dividend of $8 a share.

December 2022: Market cap $17.9B, price $50.65 per share, 354 million shares outstanding, dividend yield 15.8% per share

December 2021: Market cap $14.5B, price $49.59 per share, 293 million shares outstanding, dividend yield 16.1% per share

Using this information, net issuance in 2022 = 17.9-14.5*(50.65/49.59) = $3.09 billion dollars. Expressing this as a yield, the net issuance yield was 3.09/17.9 = 18.1% per share.

Thus IEP had outgoing dollars via dividends equal to 15.8% of its market cap in 2022, but it also had incoming dollars via issuance equal to 18.1%. More money was coming in than going out. I define the “net cash distribution yield” as the difference between these two numbers, -2.3%. I classify IEP as a cash consumer, not a cash generator, for the owners of IEP taken as a whole.

Now we are ready to address the claim that “Icahn has been using money taken in from new investors to pay out dividends to old investors.” I don’t have anything to say about “new” or “old” investors, but I’ve just shown that it is true that more money was coming in via issuance then going out to investors.

As a caution, IEP has a complex structure involving ownership by Icahn personally, leverage, and “depositary units” involving stock dividends. The idea here is that the simple formula, which just involves shares outstanding and market prices, can summarize this complex situation.

When we think of Drew’s initial reaction (“50%? I ain’t got no money in the treasury for that.”), it reminds us that there is something very real about dividends: they can’t be faked, they are actual cash money that the firm must disgorge. So investors are not wrong to focus on dividends as a value-relevant measure. Where they go wrong is focusing only on dividends and not all distributions to or from shareholders.

Are the dividends paid by IEP intentionally deceptive? I don’t know. Certainly the case of Great Northern did not involve deception, it just involved investors being confused. All I know is that investors should try not to get confused.

I recommend that you look at the total amount of cash distributed to shareholders instead of just dividends. Don’t be like Cornelius Vanderbilt! Don’t be “unaware of the increase in outstanding shares.”

Fisk is allegedly the inspiration for a Bob Dylan song, although in my view there is a regrettable lack of financial topics covered in the 9 minutes of “Lily, Rosemary, and the Jack of Hearts”.

Daniel Drew, marvelously portrayed in the movie by Donald Meek, is the originator of this pithy summary of the mechanics of securities lending: “He who sells a stock that his’n, buys it back or goes to prison.” The movie mangles this quote, replacing “buy” with “pay”. It is not enough to “pay” it back, you have to buy it back! That is the whole point of a “corner” which is

I loved the biography of Vanderbilt The First Tycoon. I especially liked the part about the primitive financial storage technology (the grandfather clock).

I won’t even talk about the most dramatic part of the movie, the events of Black Friday 1869 which involved an honest but financially unsophisticated president (U.S. Grant), allegedly corrupt presidential relatives, and enough financial shenanigans to make SBF blush.

I thank Professor Randolph Cohen of Harvard Business School for drawing my attention to this case

You may think it strange that a publicly listed stock’s legal existence would hinge of the death of a single individual, but something similar is true for Variable Interest Entities (VIEs) which are the vehicle through which many Chinese companies, such as Alibaba, listed on the US stock exchanges. VIEs involve nominees who are “natural persons” and if these individuals die or get divorced, the VIE may be at risk.

Vanderbilt didn’t enjoy being swindled, and on a different occasion he supposedly wrote following letter which is hands down the most compelling business communication in US corporate history. Twenty three perfect words:

Sadly, Vanderbilt almost certainly did not write this letter, but it remains sublime.

In reality there was skullduggery with Erie “watering down” stock and issuing possibly spurious shares, but let us supposed Vanderbilt had been able to see the share count.